Critical Illness Overview - 2015 Update

2013-Aug-29 - Rex Durington

"The prime goal is to alleviate suffering, and not to prolong life. And if your treatment does not alleviate suffering, but only prolongs life, that treatment should be stopped." - Dr. Christiann Barnard

"It's paradoxical, that the idea of living a long life appeals to everyone, but the idea of getting old doesn't appeal to anyone." - Andy Rooney

As a product of our research and client work on Critical Illness (CI) coverage, Hause Actuarial Solutions (Hause) found that there is a dearth of published material on product design and pricing for this market. There was a flurry of activity in the late 90's and early 2000's but not much of late. The state of the market is that there are as many product designs as there are carriers and a wide disparity in premium rates for roughly the same benefits. This article attempts to condense our thoughts and observations on the state of the market and the art of CI product design and pricing.

Critical Illness (CI) insurance was created by Dr. Marius Barnard, brother of Dr. Christiaan Barnard, in 1983. I won't go into the historical detail since there is sufficient literature on this topic other than to point out that the product has had a longer run and achieved a greater popularity in other countries.

That being said, Hause has noticed a significant increase in interest from providers and consumers for CI coverage in the United States over the last few years. For the interested reader, sources such as Gen Re, LIMRA and CSG Actuarial have kept score on this rapid rise in coverage and carriers.

The Market

The marketplace for CI is principally made up of Group, Individual and Worksite/Voluntary products. CI is also offered as an accelerated benefit rider on a life policy or as an additional benefit rider usually attached to a term insurance policy or combined with other health coverage.

Group and Worksite offerings require the additional complexity of setting guaranteed issue limits, rate guarantees, participation levels and portability provisions. Given the limited historical data available for CI in these markets, Hause recommends significant coordination between the distributors, actuaries, underwriters and reinsurers in setting these parameters.

According to the survey respondents to the 2011 Gen Re Critical Illness Insurance Market Survey, approximately 90% of in force policies were either voluntary worksite or individual policies. Accordingly, the primary focus of this review is the stand-alone CI product rather than CI riders. Although the thought occurs that if you renamed a rider "Critical Care" (CC Rider) you would have a ready-made theme song. How many insurance products come with their own classic rock song?

Consumer interest continues to rise as consumer driven health plans (i.e. higher consumer out-of-pocket plans) lead to costly coverage gaps and less flexibility of treatment options due to network restrictions. When the Affordable Care Act (ACA) goes into full effect in 2014, consumers will have to make many decisions concerning their major medical coverage - where to buy; how much will it cost; which plan is right for me; should I opt out entirely?

A number of insurers are getting into the market at least in part as a reaction to the confusion running rampant in the current health insurance environment. Companies that chose not to develop multiple major medical plans for the ACA may see CI as a product many people will gravitate towards. While not a substitute for major medical insurance, a well-designed CI product may be seen as a simple and affordable solution to the primary health risk most consumers recognize and fear - the financial hardship of a catastrophic or critical illness/accident.

Benefit Design

One of the key distinguishing features of CI insurance is the smorgasbord of benefit designs available. Benefits are principally lump sum payments on diagnosis or treatment for the major benefit triggers. Benefits for coverages shown below in the "Other Benefit Triggers" category generally have a fixed dollar limit.

A minimalist plan by today's standards would be one that covers Heart Attack, Stroke and Invasive Cancer. These plans were often filed as specified disease or dread disease policies. Subsequent enhancements added major organ transplants and end-stage renal disease.

Today's offerings include the following menu of benefit triggers:

| CI Benefit Design Triggers | ||||

| Invasive Cancer | Heart Attack | Stroke | ESRD | Major Organ Transplant |

| Coma | Paralysis | Severe Burns | Loss of Sight, Speech, Hearing | Alzheimer's Disease |

| ALS (Lou Gehrig's Disease) | Benign Brain Tumor | Occupational HIV/Hepatitis | Quadriplegia | Multiple Sclerosis |

| Loss of Limbs | CABG (By-Pass Surgery) | Angioplasty | Stent | Carcinoma in situ |

| Prostate Cancer | Skin Cancer | Laser Relief | Consultation Benefit | Hospital Confinement |

| Radiation/Chemotherapy | Loss of Independent Living | Bone Marrow Transplant | ||

| Additional Child Triggers | ||||

| Cerebral Palsy | Cleft Lip/Palate | Cystic Fibrosis | Down Syndrome | Spina Bifida |

| Acute Respiratory Distress Syndrome | Type I Diabetes | Muscular Dystrophy | Congenital Heart Disease | Child Care Expense |

| Other Benefit Triggers | ||||

| Wellness Benefits | Cancer Vaccine | Ambulance Transportation | Hospital Admission Benefit | Hospital Confinement Benefit |

| Air Transportation | ICU Confinement | Follow-up Care | Health Screenings | Lodging |

If the above list is not daunting enough, there are also variations by benefit trigger on the percentage of the policy paid or dollar limits by benefit. Some product designs group the benefits by category and apply limits within each benefit category. Invasive Cancer is most often priced separately to allow marketing flexibility and avoid duplication of coverage. State requirements may also dictate particular benefit trigger inclusion or exclusion.

Popular optional benefits include return of premium and recurrence benefits on a full or partial basis. Recurrence benefits are usually structured to allow for 50%-100% of the original coverage to be paid for a recurrence of a covered benefit trigger. A distinction is usually made between the same diagnosis or a different diagnosis and the length of time between occurrences. Also, some benefits such as Cancer In Situ may be excluded or limited to one occurrence under the policy.

In designing the benefits, it should be kept in mind that the various triggers will appeal to different demographics. The younger crowd won't be as concerned with heart attacks and stroke as with triggers that may occur due to an accident - paralysis, coma, etc.

There also is the philosophical (and sometime regulatory issue) of what constitutes a "Critical Illness". Many of the benefits above may not be considered "critical" to either the consumer or regulators. Regulators are also concerned that certain benefit triggers may falsely lead consumers into believing they are buying comprehensive medical coverage rather than CI.

Benefit design should also consider the abilities/constraints of the underwriting, compliance, claims and actuarial departments. More complex designs require a longer application and a lengthier filing process. Claims departments have to adjudicate each claim against a menu of triggers and benefit limits. At some level of product complexity, the pricing actuary will run out of credible data. "Actuarial judgment" usually translates into long talks with regulators - without a walk on the beach.

Under HIPAA there are "excepted benefits" exemptions which avoid minimum loss ratio (80%-85%) and unlimited annual and lifetime benefits requirements of the ACA. The essential exemption provisions are:

- benefits for medical care are secondary or incidental to other insurance benefits

- offered as independent, non-coordinated benefits

- coverage only for a specified disease or illness, hospital indemnity or other fixed indemnity insurance

- coverage is provided under a separate policy, certificate, or other fixed indemnity insurance

- benefits are paid for an event regardless of whether benefits are provided for the same event under any group health plan maintained by the same plan sponsor

In order to be hospital indemnity or other fixed indemnity insurance, the insurance must pay a fixed dollar amount per day (or per other period) of hospitalization or illness, regardless of the amount of expenses incurred and not a per service benefit.

One of the key distinguishing features between CI plan designs is the benefit reduction or termination age. The most common reduction noted in Hause's research was 50% at age 70 or 75. Variations range from termination at age 65 to no reduction of benefits with advancing age. This design feature will significantly impact claims costs and reserves; and therefore premium levels. Here again, differing state regulations may require multiple plan designs as some states restrict reduction by age.

Spouse and Child Coverage, if offered, may be individually priced or family mix priced. Child rates may be for each child or an all children rate. Spouse and child benefit limits are often limited to a percentage (50% spouse, 25% children for example) of the primary insured's coverage or a dollar maximum.

Waiting periods are normally zero or 30-days and pre-existing exclusion are not covered for 6-24 months (optionally selectable in some cases). Look back periods vary by state with six months being the most frequent limit.

Hause sees this morass of benefit triggers and features as overloading a simple and practical product. The menu of options will also probably overwhelm most pricing actuaries. The extra marketing pizazz of additional benefit triggers is probably lost on the consumer and may be detrimental to sales if the consumer feels they are paying for more than they want or will likely use. Extra complication in the plan design will also lead to more difficult, costly and time-consuming state filings.

Underwriting Criteria

Group coverage generally excludes health questions (other than tobacco use) except for late entrants or those applying for higher amounts than the guaranteed issue limits. Employee-pay plans are more similar to the individual and worksite products.

Worksite and Individual products often use simplified underwriting of seven or fewer health questions beyond age, gender, height and weight:

- AIDs Question

- Cancer Question

- Heart Question

- Transplant-related Question

- Organ transplant generally refers to Kidney, Lung, Liver and Pancreas.

- Family History

- Have two or more parents or siblings ever been diagnosed or died from a benefit trigger before the age of 45/55/60?

- Tobacco/Nicotine Question

- Typically within 12 months on an "any usage" basis.

- Employment status (worksite/group products)

- Actively at work

- Hours worked per week

- Missed more than 5 consecutive days due to illness or injury

Additional questions generally relate to expanded benefit triggers such as asking whether help is needed with activities of daily living (ADLs) as a condition for a Loss of Independent Living benefit.

Wording variations in applications have also been noted. The questions may relate to whether the person ever (or within 2-10 years depending on insurer):

- Been diagnosed

- Been medically advised

- Sought treatment

- Had surgery

- Had an indication, sign or symptom of a listed condition.

"Ever had" language may be restricted in many states.

Regulatory Issues

Regulatory issues associated with CI filings may be separated into forms issues and rate issues.

- Forms IssuesThe most common State variations key on definitions and benefit limitations. "First occurrence" and "first diagnosis" language may be considered in conflict with waiting period and pre-ex limits in a number of states.States also vary on their allowance and treatment of waiting periods and how to handle diagnoses during the waiting period. Some require a reduced benefit or a return of premium while other states may not allow a waiting period.Pre-existing condition restrictions vary as to whether they are allowed, the length of time allowed for look-back and the length of time they may be excluded.Other state variations include:

- Issue age restrictions to age 65

- Whether benefit reductions are allowed

- Mandated benefits or provisions - mammography, breast cancer, preventive care

- Rate IssuesWhile a "generic" pricing model may be used in most states, a number of state variations will require special treatment. A recent Hause CI filing resulted in about 60% of the states fitting the generic model with the balance requiring some state specific pricing.Variations:

- Loss Ratios (50%-60%)

- Benefit reduction variations

- Benefit trigger inclusion/exclusion

- Issue Age ranges

- Mandated benefits

Premium Rate Comparison

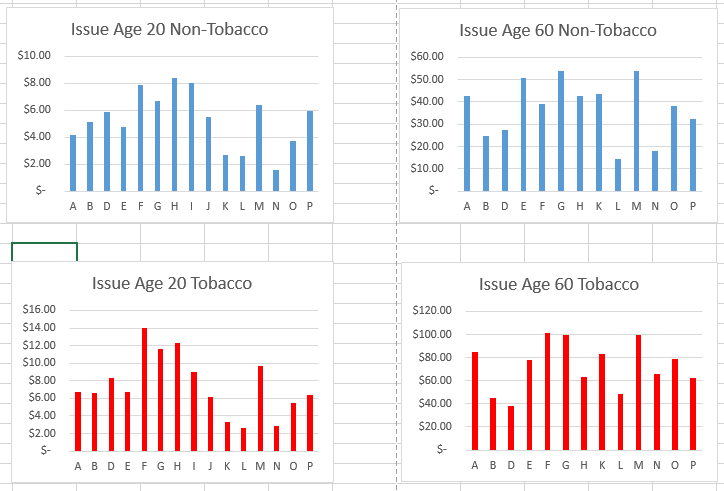

As the accompanying charts show premium rates vary substantially between companies. Some of this variation may be explained by marketing method and benefit design differences between plans. Hause believes a substantial portion of this variation is due to the immaturity of the market and/or scarcity of companies offering comparable plans.

Currently, competition is not as much on price, but on which trigger appeals to each particular insured or group. Despite the ubiquitous duck commercials, prospective insureds are not aware of the variety of CI product features or relative prices. They generally will not look at more than one CI product (especially in worksite or group environments). This helps explain why there are so many varieties of CI insurance on the market at markedly different premium rates.

In looking at the premium split for cancer coverage versus all other benefits it was found that cancer coverage represents roughly 50% of the total premium rate for most carriers. Heart-related triggers accounts for about 35% of premium, organ-related (ESRD and transplants) about 10% with the balance to other benefits. The percentages by carrier are also relatively consistent by issue age.

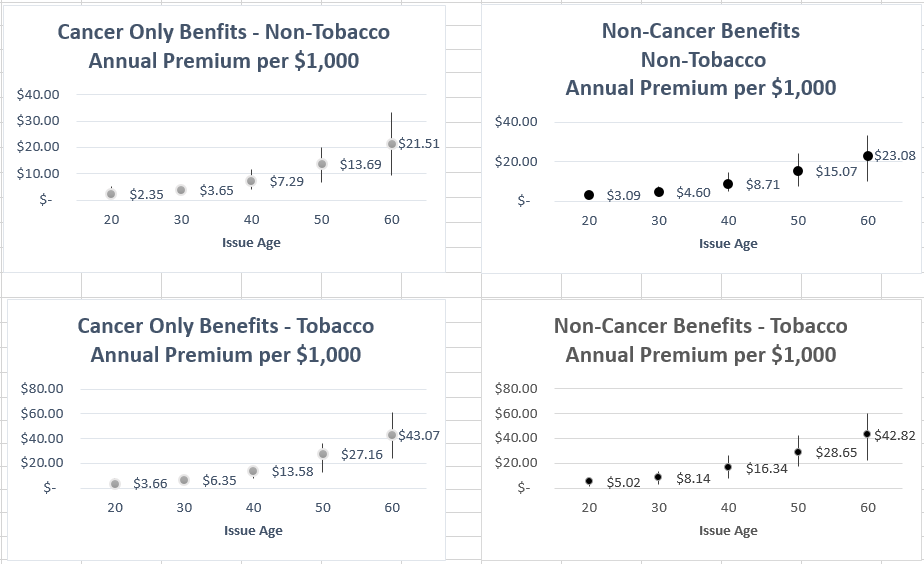

The following charts show the average high and low premiums for cancer only and other than cancer benefits by issue age. The dispersion increases with advancing age due primarily to variations in claim costs and benefit differences at the older ages. Also, it should be mentioned that care needs to be taken when comparing different carrier rates as benefits may be paid only for the first occurrence of any trigger, limited by maximums within a trigger category or otherwise restricted such that benefit pieces (cancer versus non-cancer) are not additive.

Wellness benefits or health screening benefits generally provide a $50 annual payment if the insured(s) have a preventive care test or procedure. The premium for this benefit was found to range from $15 to $40 with the most typical rate being about $20 without regard to issue age or tobacco usage.

Subsequent diagnosis/recurrent benefit premium rates vary by the included coverages, percentage allowed on recurrence and provisions for the same trigger (reoccurrence) or a different trigger (recurrence). As mentioned earlier, design variations also exist on the required time to elapse between occurrences.

The table below show the approximate percentage adjustments for a 100% recurrent benefit provision. In general, the probability of recurrence is highest for heart-related triggers.

| Approximate Recurrence Adjustments | ||

| Issue Age | Without Cancer Coverage | With Cancer Coverage |

| 20 | 8% | 11% |

| 30 | 11% | 13% |

| 40 | 17% | 24% |

| 50 | 20% | 24% |

| 60 | 20% | 24% |

Caution is in order here. There is significant interplay between the recurrent benefit provision and the reduction in benefits at advancing age provision (if any). Product pricing will most likely entail extensive testing of the mix between these benefit provisions, the expected distribution of business by age and competitive considerations.

Reduction in benefit provisions naturally impact the higher issue ages more than the earlier issue ages. If the target market is in the younger ages, a steeper benefit reduction provision may be added to the design to lower premium rates slightly without sacrificing key benefits. However, if the target market is older, the attractiveness of the coverage may decrease with a steep benefit reduction.

The following table shows the approximate percentage change in premium rates of a reduction of benefits by 50% at age 70 versus a plan with no reduction in benefits.

| Approximate Percentage Change due to a 50% Benefit Reduction Factor at Age 70 | |

| Issue Age | Percentage Adjustment |

| 20 | 2% |

| 30 | 4% |

| 40 | 6% |

| 50 | 10% |

| 60 | 20% |

| 65 | 33% |

Given the significant percentage impact at the older issue ages, a viable approach to benefit design would be to begin with an age 65 pricing target and work backward from there.

Closing

CI Insurance, while still not fully developed in the U.S. market, shows promise as a product that can fill costly out-of-pocket gaps in health coverage. It is attractive to the "young invincibles" as catastrophic coverage and to the rest of us as income protection from high deductibles, lost income and other costs that arise with an unexpected catastrophic illness or accident.

While potentially intricate in design and pricing, the product concept is simple. One-stop shopping for protection against the illnesses we all fear the most. The key point in CI product design and pricing being to follow Occam's Razor - keep it simple. Your policyholders will thank you and your actuarial, underwriting, compliance and claims departments will thank you.

Finally, if you have made it this far, a final quote:

"I'm the only M.A.S.H. character covered by a Critical Illness policy." - Major Burns.

Couldn't resist the last one. Actuarial humor - never gets old, never gets funny